{kind=link}

In accordance with information from buying and selling agency Webull, round 70% of Grayscale GBTC holders doubtless stay in revenue. The typical shares have been bought at $27.82, some 20% beneath the present value as of press time.

The Webull information exhibits the state of the belief the day earlier than its conversion to a spot Bitcoin ETF and signifies that 70% of buyers had a value vary between the $18.84 and $27.24 vary.

When it comes to distributions, the primary focus of shareholders seems to be positioned between $33 and $40. With the worth at $34.9 as of press time, will probably be attention-grabbing to see whether or not the underside of this vary acts as a help for the worth amid continued outflows.

The second focus is way decrease, between $18 and $21. This group will stay worthwhile till the GBTC value falls one other 39%.

Ought to the worth fall to this degree and its belongings beneath administration see an equal decline, we’d witness an additional 230,000 BTC hit the OTC desks, price round $8.9 billion as of press time.

Such a drop would depart Grayscale with roughly 350,000 BTC, which at a 1.5% administration charge would nonetheless generate roughly $200 million in income if Bitcoin retained a price of round $39,000. This underlines the dearth of stress on Grayscale to decrease charges together with the seemingly limitless potential for Grayscale buyers to take income. With few inflows into the ETF, the proportion of buyers in revenue could be very excessive.

Thus, there may be definitely an argument to be made that Grayscale’s stress on Bitcoin’s value via profit-taking may very well be as extreme as a near-40 % drawdown. For bears within the viewers, a 40% drop for Bitcoin proper now would take it to Might 2023 lows of roughly $23,000.

Probably 100% of Grayscale buyers in revenue at conversion.

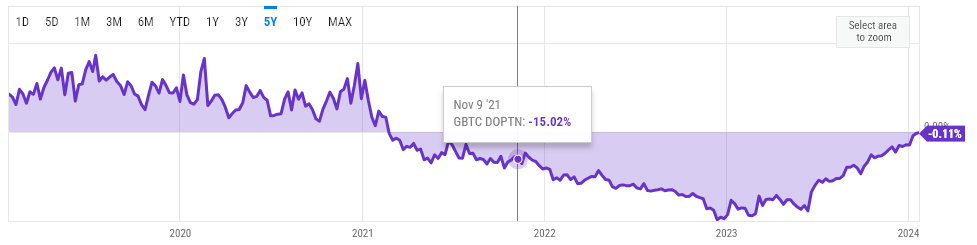

Since its conversion, the ETF has seen appreciable outflows totaling roughly $3.5 billion. Its belongings beneath administration have additionally fallen to $22.1 billion (552,681 BTC) from a year-to-date excessive of $29 billion (623,390 BTC) on Jan. 10. In greenback phrases, its AUM all-time excessive was really additional again, aligning with the highest of the 2021 bull market at a staggering $44 billion (651k BTC.)

Curiously, even on the prime of the market, issues concerning the belief’s make-up resulted in it buying and selling at a 15% low cost to its web asset worth (NAV), representing a value prime of round $58,000 as a substitute of the spot value of $69,000. This low cost continued to extend till the beginning of 2023, reaching -47% at its lowest.

By way of the appliance and eventual success of its conversion to a spot Bitcoin ETF, the low cost has all however disappeared to a mere -0.11% as of Jan. 23.

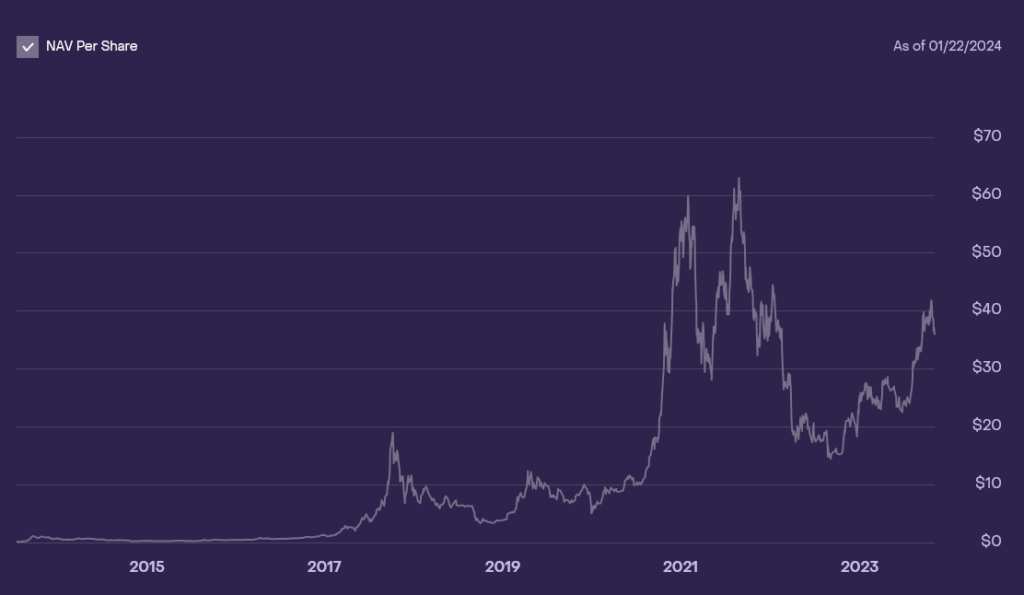

Curiously, the place value distribution chart from Webull above signifies that every one buyers who purchased about $40.53 exited the belief earlier than its conversion. In contrast with the chart beneath of the historic NAV value, GBTC principally traded above $40.53 for round 12 months between Might 2021 and Jan. 2022. Nevertheless, Webull information counsel that when the belief closed on Jan. 10, its final day earlier than its conversion to an ETF, 100% of shares have been worthwhile.

The TradingView chart beneath helps this declare, because it closed out at its highest value in 17 months. What’s extra shocking is the variety of buyers who had already exited the fund after having entered at larger costs all through 2021.

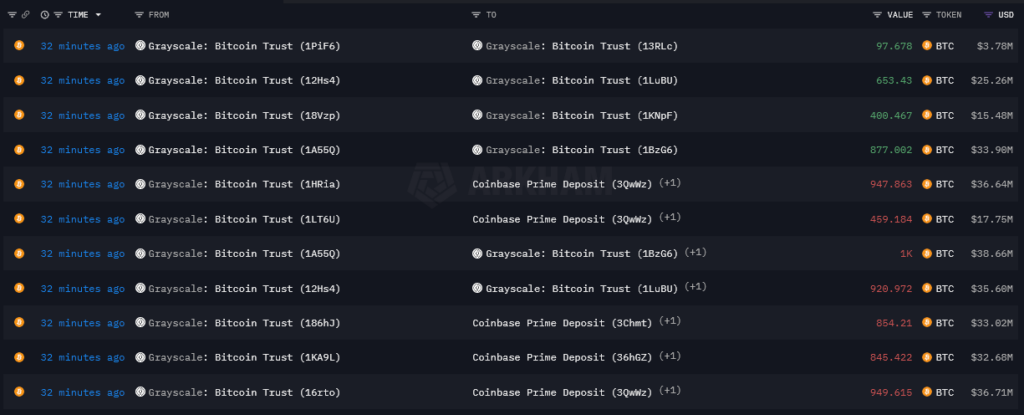

Following the revelation that a lot of the outflows from GBTC have been a results of FTX liquidations, many within the Bitcoin group have been buoyed by the prospect of the ETF outflows slowing down. Nevertheless, an additional 17,000 BTC was despatched to Coinbase Prime immediately, Jan. 23, with web outflows of round 15,000 BTC, valued at roughly $600 million.

The excessive variety of buyers in worthwhile positions places the ETF in a precarious place for additional outflows. But, the impression it will have on the spot Bitcoin value will solely be seen with time. Trades between the ETF issuers and its buying and selling counterparty, Coinbase, occur over-the-counter. (OTC), thus having a restricted impact on the underlying Bitcoin value instantly.

Nonetheless, that is solely true so long as there are consumers prepared to accumulate Bitcoin. Ought to the OTC liquidity dry out, the worth impression may very well be monumental. Nevertheless, given the institutional demand for Bitcoin, I can’t think about buyers like Michael Saylor turning down the possibility to accumulate some low-cost Bitcoin.