{kind=link}

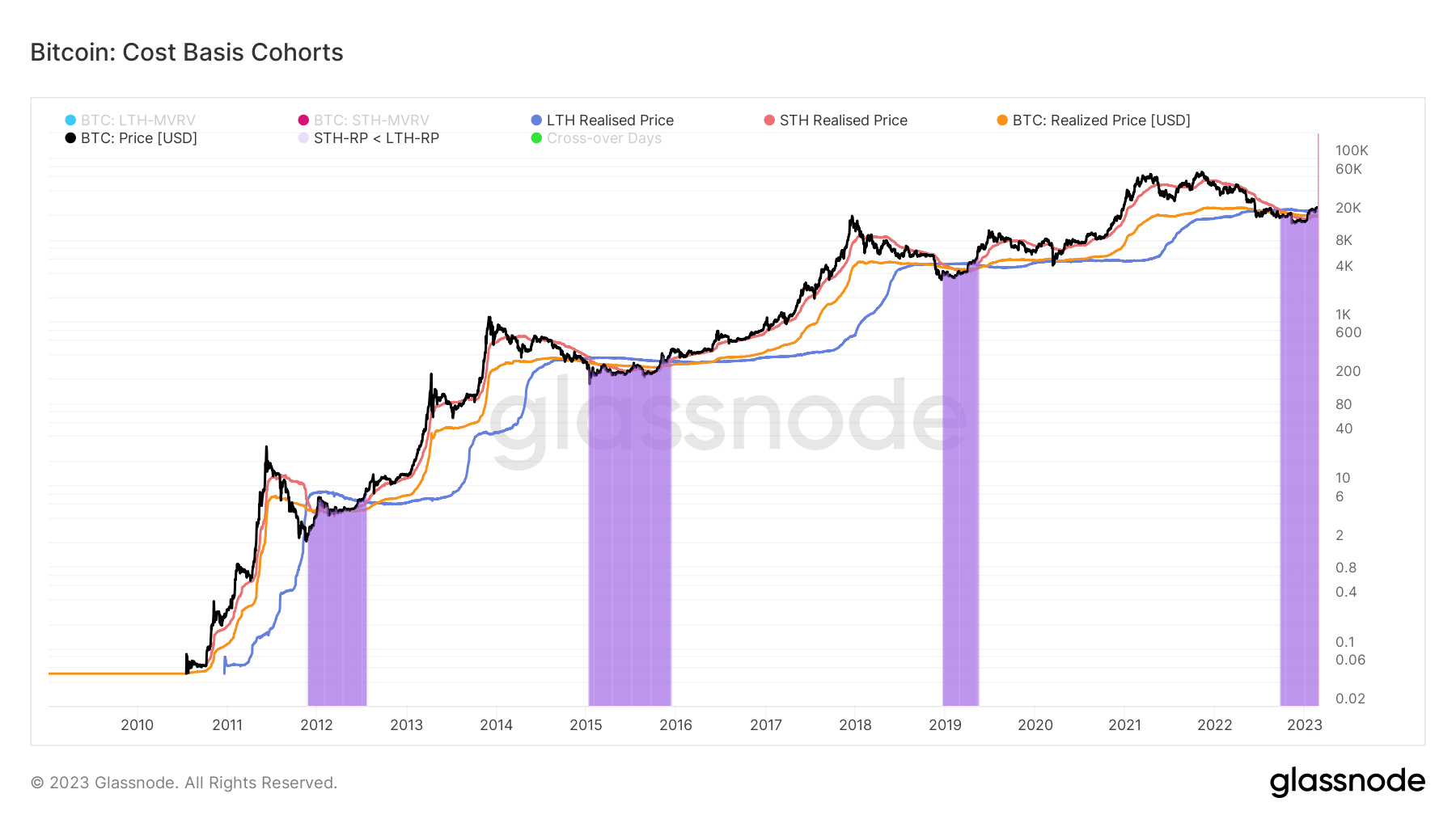

Realized value is a metric typically used to find out market actions in bear and bull markets. Outlined as the worth of all Bitcoins on the value they had been purchased divided by the variety of circulating cash, realized value successfully exhibits the cost-basis of the community.

Dividing the community into cohorts can assist us mirror the mixture value foundation for every main group proudly owning Bitcoin. Lengthy-term holders (LTHs) and short-term holders (STHs) are the 2 main cohorts driving the market — LTHs are all addresses that held BTC for longer than 155 days, whereas STHs are addresses that held onto BTC for lower than 155 days.

The LTH-STH value foundation ratio is the ratio between the realized value for long-term and short-term holders. Given the traditionally completely different behaviors LTHs and STHs exhibit, the ratio between their realized costs can illustrate how the market dynamic is shifting.

For instance, an uptrend within the LTH-STH value foundation ratio is seen when STHs notice extra losses than LTHs. This exhibits that short-term holders are promoting their BTC to LTHs, indicating a bear market accumulation part led by LTHs.

A downtrend within the ratio exhibits that LTHs are spending their cash sooner than STHs. This means a bull market distribution part, the place LTHs promote their BTC for revenue, which STHs purchase up.

An LTH-STH value foundation ratio larger than 1 signifies that the fee foundation for LTHs is larger than the fee foundation for STHs. This has traditionally correlated with late-stage bear market capitulations that become bull runs.

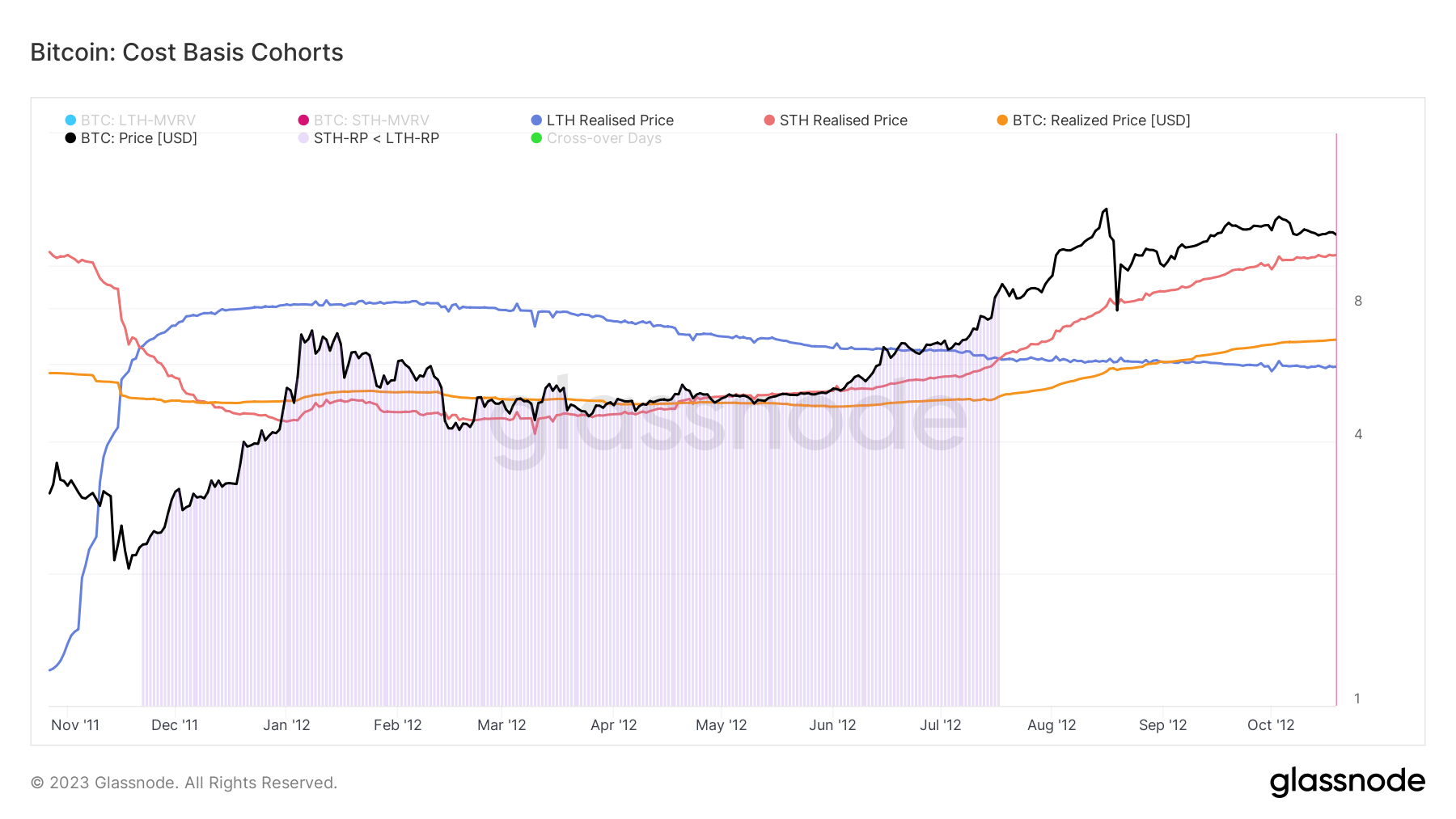

2011

Throughout Bitcoin’s first bear market in 2011, the STH realized value went under the LTH realized value. This pattern reversal marked the start of a bear market which began on Nov. 22, 2011 and lasted till Jul. 17, 2012.

Lengthy-term holders collected BTC all through the bear market, dollar-cost averaging (DCA) and bringing their cost-basis down. Shopping for throughout suppressed costs created a brand new inflow of short-term holders that pushed Bitcoin’s value up. This improve in STH accumulation brought on the STH realized value to rise, growing the general cost-basis of the community with it.

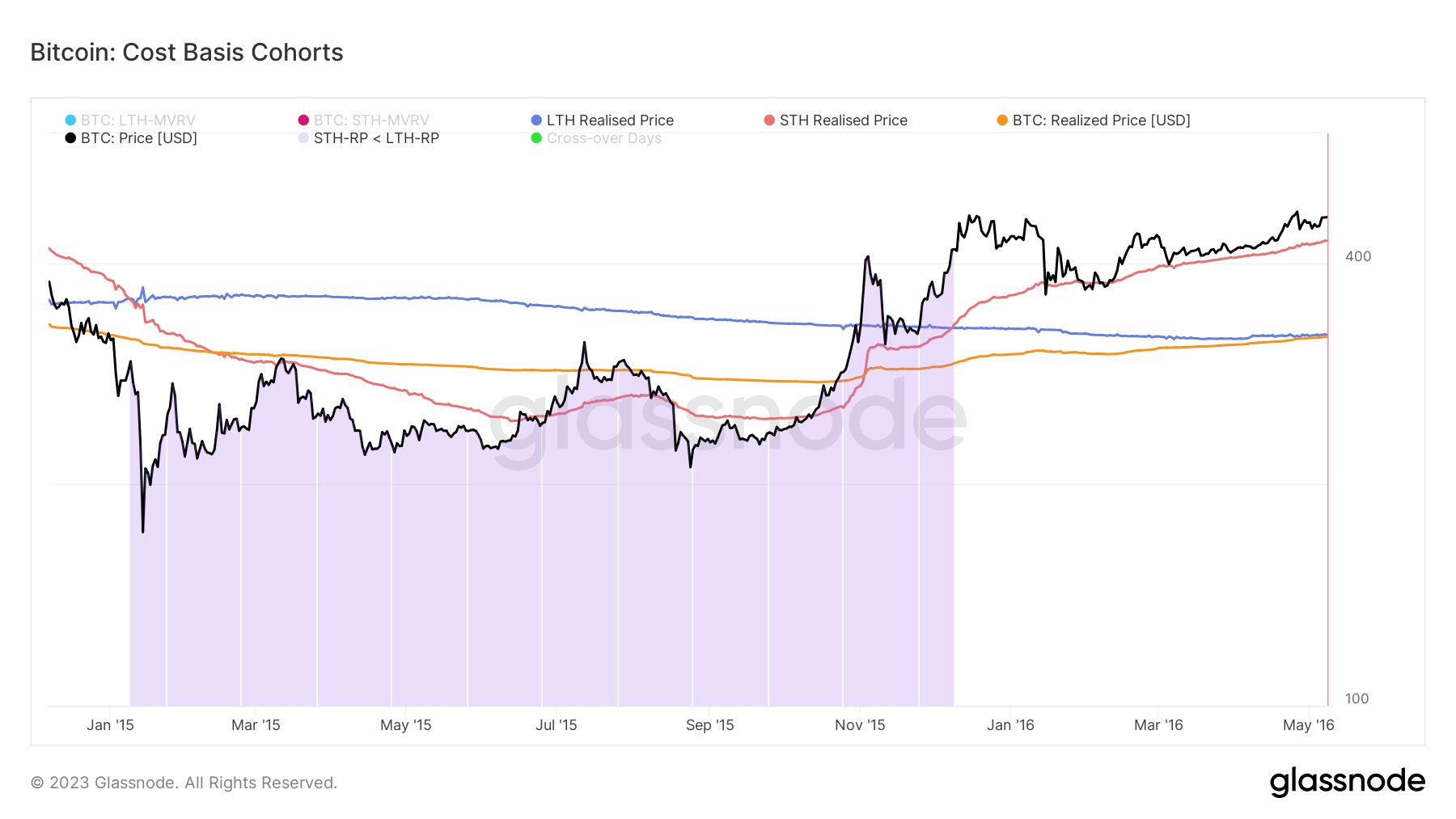

2015

The 2015 bear market adopted an analogous sample. On Jan. 8, 2015, the STH realized value dropped under the LTH realized value, triggering a bear market that lasted till Dec. 08, 2015.

Whereas Bitcoin’s value started recovering in early November 2015, it wasn’t till the start of December that the STH realized value broke above the LTH realized value. On the time, the general value foundation of the community elevated barely, triggering a bear market reversal that noticed Bitcoin’s value go previous $400.

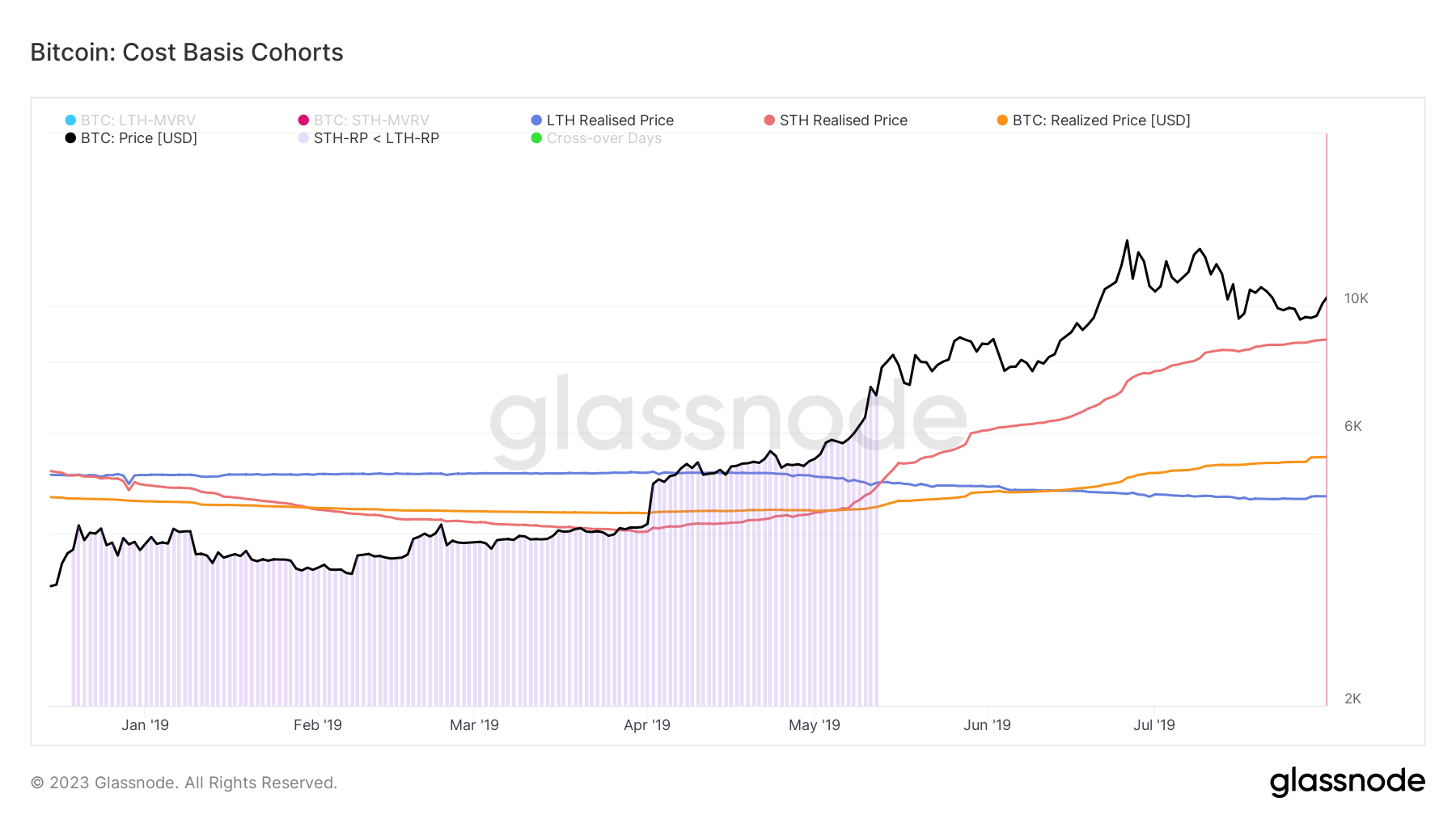

2018

Bitcoin’s coveted rally to $20,000 in late 2018 ended when the STH realized value declined. It dropped under the LTH realized value on Dec. 20, 2018, pushing Bitcoin’s spot value approach under its realized value.

The bear market ended on Could 13, 2019, when the STH realized value bounced again above the LTH realized value.

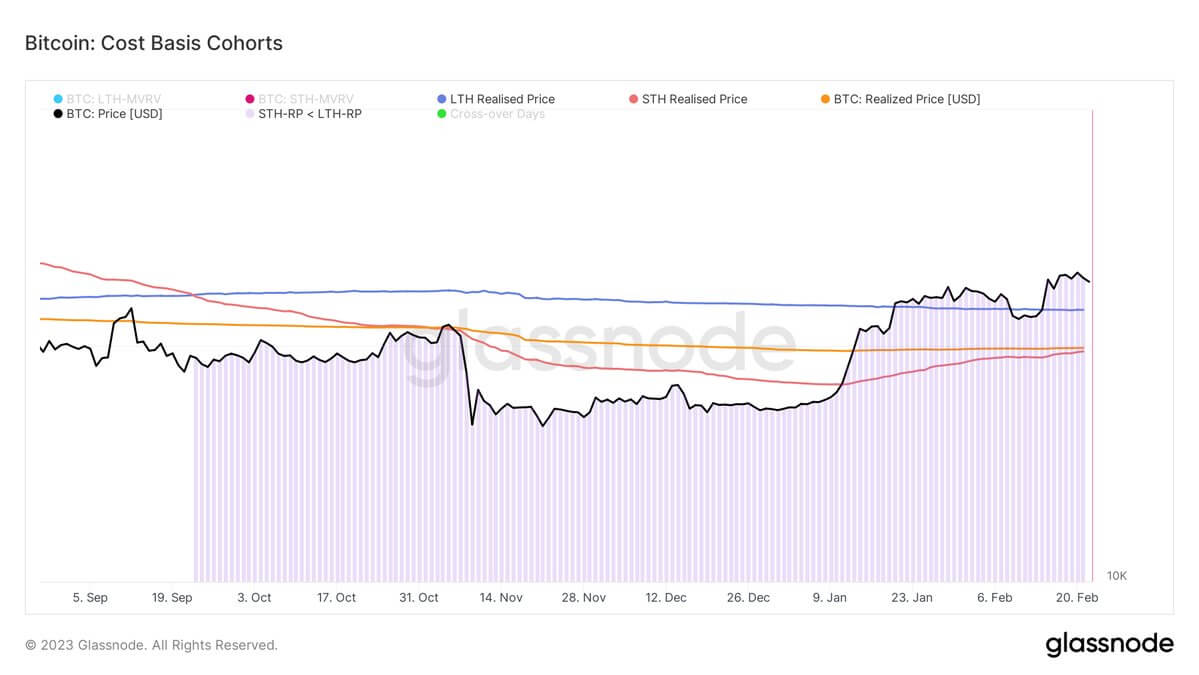

2022

The STH realized value started descending at first of September 2022, dripping under the LTH realized value on Sept. 22, 2022. It continued downward till Jan. 10, 2023, when it started a sluggish and regular rebound that just about introduced it on par with Bitcoin’s realized value.

The STH realized value at the moment stands at $19,671, whereas the LTH realized value is $22,228. Bitcoin’s realized value is $19,876.

Information analyzed by StarCrypto confirmed that 4-year cycles within the Bitcoin market finish when the STH realized value flips each Bitcoin’s realized value and the LTH realized value. This creates a measurable market FOMO that triggers a parabolic run.

This flippening occurred in 2011 after 9 months in a bear market, in 2015 after 11 months, and in 2019 after 6 months. It’s been 5 months because the STH realized value dropped under the LTH realized value in 2022.